Mounted or adjustable variable charge mortgage, choose the higher one when taking a mortgage you make a 30-year lengthy determination, resolve correctly.

Picture supply: YouTube Video Screenshot

Mounted or (Adjustable) Variable Fee Mortgage in 2019 – Choose The Higher One

Get The Full Sequence in PDF

Get all the 10-part collection on Charlie Munger in PDF. Reserve it to your desktop, learn it in your pill, or e-mail to your colleagues.

Q3 2019 hedge fund letters, conferences and extra

Transcript

Good day fellow investor. So my inventory markets analysis platform, I just lately acquired a really, superb questions on whether or not to choose a hard and fast or adjustable variable charge mortgage. And I actually need to give my perspective on that to assist. I am positive there are a variety of you who’re fascinated with that. My message is, watch out, you are making a 30 yr lengthy monetary life determination when taking a mortgage often of 40 years. And folks often have one month or one espresso perspective that they’ve with their mortgage advisor when taking such an funding when making such a call. So 40 yr lengthy, you must actually have a long run perspective on that. And that is what I will provide you with.

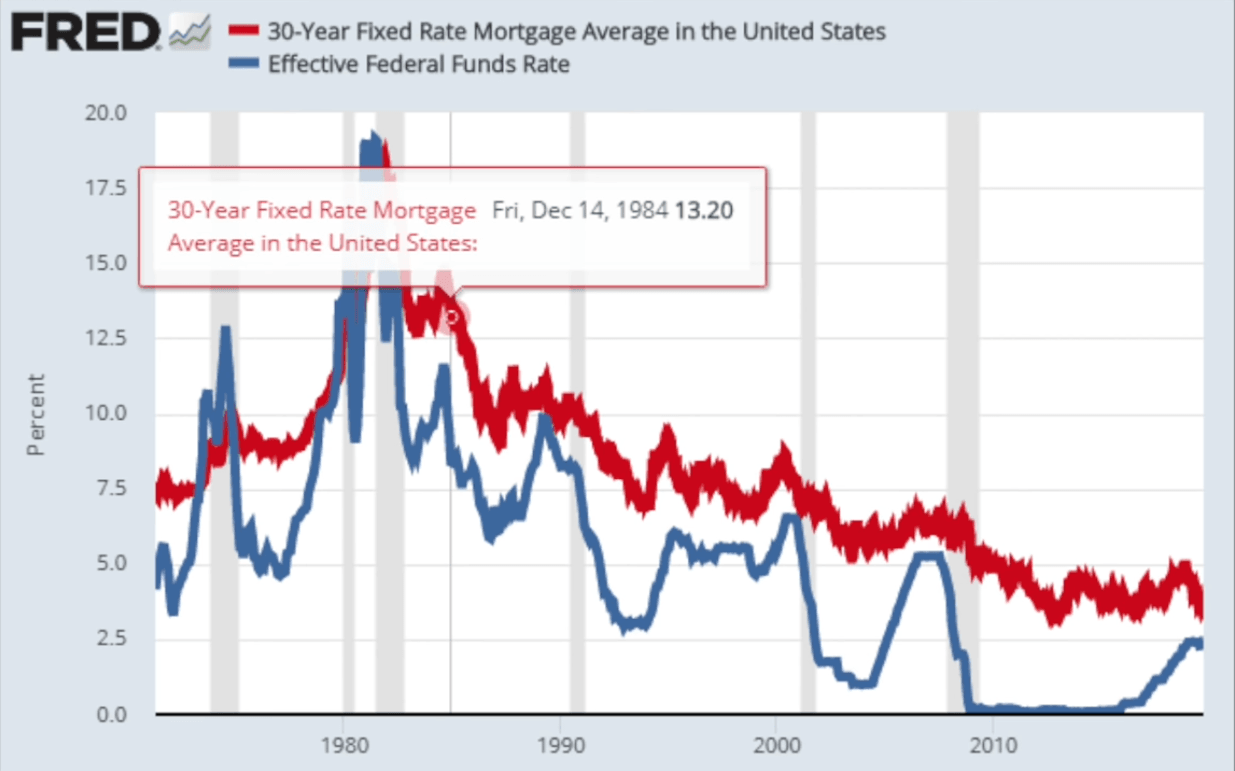

We’ll focus on the distinction, the dangers, the funds, examples, and you then’re going to verify and you then’re going to have the ability to make a very educated determination on what’s higher for you. Let’s begin. So a variable rate of interest or adjustable rate of interest modifications in relation to how the market rates of interest change, your mortgage would in all probability have an rate of interest that could be a bit greater than the rate of interest mentioned. However the central financial institution rates of interest are right here. On the blue, you see the 40 yr mortgage charge all the time a bit of bit greater. The adjustable charge is in between these charges, and they’re decrease often than the 30 yr mortgage charge.

What’s vital from this image is that the 30 yr mortgage charges have additionally been above 13% over an extended interval of greater than 4 years within the 1980s. So that could be a threat that in the event you take an adjustable or variable charge, you would possibly see charges 5, 6, 7, eight, 10, 15% over the subsequent 40 years. It wasn’t that way back, the mortgage is what the 7% and now however now many assume it’s not possible. So do not take issues with no consideration as these are actually and I am going to present you later how issues would possibly change within the prices that you’re paying the fastened rate of interest mortgage, in the event you don’t love uncertainty in the case of a month-to-month funds, you’ll take a mortgage with a hard and fast rate of interest.

Mounted vs adjustable variable charge

That ought to not change over the entire course of the mortgage plus, at the moment, actually now, you see the massive volatility in these charges 355 % three.5. Now some actually low historic lows, and that is why I am pushing for a 30 yr, 30 yr not 10, not 20, 30 yr fastened mortgage charge.

The detrimental facet of the fastened mortgage charges is that charges and that is the price of your month-to-month cost is often greater than what variable charges a financial institution has to insure towards modifications in rates of interest for the subsequent 40 years and subsequently studies the next charge the purple one is the 30 yr fastened mortgage charge and the blue one is the adjustable charge there may be all the time a 1 share 2 share factors distinction not Presently, however it can in all probability once more, regulate to debt.

However, let’s take 1% level distinction and on an 80ok mortgage that you simply want in the US to purchase 100ok house, it is $50. In order that’s the price of taking a hard and fast charge mortgage and sleeping effectively over 40 years now, okay $50 you may have a decrease cost with adjustable charge or greater cost with a hard and fast mortgage charge.

Small is loads with mortgages

The distinction is that they made calculation for the Netherlands are even decrease than this as a result of the rates of interest are down there from 1.25 variable adjustable to 2.5 30 yr mortgage. That is actually loopy. And nonetheless persons are taking the adjustable even when the distinction is 10, 20, 30 euros on a 100,000 mortgage. That is loopy to me.

Let me put issues into perspective. To illustrate you’re taking an 80ok mortgage, you’re taking an adjustable charge of three.6% on it, the charges stay fastened for 10 years however you then to inflation charges spike 10%. On an 80ok mortgage after 10 years, you pay down solely $15,626 of your principal as a result of it’s important to first pay curiosity in your mortgage. The remaining stability is what it’s important to pay over the subsequent 20 years. if rates of interest spiked to 10%, you continue to have 20 years to return 64,000 the month-to-month cost charge of 10% can be 742 or 47% greater than the present one.

In the event you take an adjustable charge that’s the threat for taking adjustable mortgages. You by no means know what lies forward and even 10 yr fastened mortgages. If rates of interest go even greater, then you might be actually screwed. So that is the distinction in prices between taking a hard and fast.

source https://jobsearchtips.net/mounted-or-adjustable-variable-fee-mortgage-choose-the-higher-one/

No comments:

Post a Comment