Alternative Equities Fund letter to traders for the third quarter ended September 30, 2019.

Q3 2019 hedge fund letters, conferences and extra

Pricey Investor:

Markets have been up and down in Q3. The massive caps once more continued their outperformance over small caps, because the S&P 500 added +1.7% to year-to-date beneficial properties whereas the Russell 2000 gave again -2.four% for the quarter. Our portfolio was up +5.5% within the quarter. This newest replace now means $1 invested in our portfolio since turning into unbiased in 2017 is value $1.58 versus our Small/Giant blended benchmark of $1.22.

Govt Abstract

On this letter, we spotlight Bluelinx (BXC) and The Rubicon Challenge (RUBI) because the notable efficiency drivers for the quarter. We then focus on new portfolio additions At Residence (HOME) and Quantum Corp. (QMCO) earlier than closing with just a few ideas on our funding outlook.

Notable Efficiency Drivers

This quarter’s optimistic efficiency got here from a portfolio that seemed slightly lopsided at occasions. At one level, our largest place was an nearly 30% holding in money, adopted in measurement by our place in The Rubicon Challenge. Mixed with three different “core” positions sized round ~10%, a number of smaller ones and some small hedges, our internet publicity touched as little as ~60% for some stretches of the quarter. So, for the very transient 90-day interval that was Q3, this posture mixed to create the supposed consequence: our portfolio returns have been largely pushed by our chosen shares and fewer so by the markets through which they commerce.

Bluelinx shares carried out properly within the third quarter as the corporate continues to make regular progress integrating their extremely accretive Cedar Creek acquisition. Final winter’s lull in housing market exercise is proving to be simply that, as single-family begins are once more rising attributable to regular structural demand and the current impetus from decrease rates of interest. As we prompt in our prior letter, the corporate seems to be at an inflection level. Administration appears to agree, with CEO Mitch Lewis stating on their final earnings name that they count on “the second quarter will prove to have been an inflection point for our company.” Continued tailwinds from a rising housing market ought to do wonders for the corporate to allow their sturdy money movement technology means to shine via. With continued regular execution on the synergy case, we expect it’s potential traders will see as a lot as $9/share of annualized free money movement within the coming quarters.

The Rubicon Challenge can be performing properly. The 2Q report was the third consecutive quarter to function 30%-plus topline progress and got here with a equally sturdy outlook for the upcoming quarter. The above market progress has been pushed by continued share beneficial properties from smaller subscale supply-side platforms in each desktop and cell verticals. Rubicon has additionally had essential wins in excessive progress codecs like video and audio. Current product introductions like nToggle and Estimated Market Charge have made their environment friendly platform extra engaging to publishers, and the corporate seems to have yet one more share-winning product within the pipeline. In September, I had the pleasure of attending the corporate’s demo occasion for its new Demand Supervisor providing at their New York workplaces. The product is a brand new suite of analytical instruments that overlay the Prebid open-source software program platform the corporate was instrumental in constructing. The user-friendly product lowers the associated fee for publishers to judge and analyze the ROI related to their advert stock throughout all promoting codecs. Although it’s early, suggestions has been fairly optimistic, and the providing appears to have been a contributor to new buyer wins. With continued iterative enhancements in product choices and scale benefits over smaller friends, the corporate seems properly positioned to meet ’s want for a powerful unbiased, omnichannel, international supply-side trade.

Portfolio Exercise

Within the quarter, we exited Chipotle, one among our core positions, and changed it with At Residence as a brand new core place. We additionally added Quantum within the particular scenario bucket.

CMG – After practically tripling in just below the final two years since we initiated our place, we accomplished our exit of Chipotle in Q3. CEO Brian Niccol has the corporate firing on all cylinders. Improved advertising and marketing, supply growth, digital initiatives and continued new retailer progress have enabled the corporate to efficiently full its turnaround. Chipotle is now again to taking part in offense. Buyers appear to agree the longer term is shiny and have rewarded the sturdy execution by bidding shares as much as a degree that now not meets our margin of security or anticipated return thresholds. Accordingly, we exited the place.

HOME – Little greater than a 12 months in the past, At Residence was thought to be a high-quality progress inventory with a profitable and differentiated method to brick and mortar retailing. The furnishings and décor retailer had garnered investor favor for its differentiated enterprise mannequin that received over shoppers with its large breadth of merchandise (usually 50,000 SKUs per retailer) and engaging value factors (usually 15 – 25% decrease than friends like Wal-Mart or Wayfair). Good sourcing of personal label merchandise and a lean low-cost working mannequin serving clients from large field shops (usually ~100,000 sq. ft) generated sturdy unit economics and engaging returns on capital. The corporate’s sturdy share beneficial properties and rising retailer base positioned the retailer as one thing of a category-killer. Since coming public in 2015, the corporate was one among only a handful of shops to put up uninterrupted optimistic comps and an earnings CAGR within the mid-20s proportion degree for the final three years.

However occasions and sentiment modified swiftly this previous 12 months. The brief model of the story is that this: first progress investments, then tariffs and subsequently softening comp developments all culminated in a nasty confluence of occasions that wreaked havoc on the corporate’s near-term earnings progress trajectory. Attributable to these components and another one-time occasions, GAAP financials now paint the image of progress interrupted, with a extreme dent impaled into the corporate’s rising earnings stream. Development traders would subsequently abandon this one-time darling, sending shares to ranges that appear to counsel these points are totally everlasting.

Our analysis suggests in any other case. We consider most of those unfavorable developments are non permanent and sure parts of the corporate’s enterprise mannequin are merely misunderstood. After a deep dive bolstered by a gathering with administration at their Plano, TX headquarters and conversations with a number of former staff, we consider the corporate’s current course correction and downshift in close to time period unit progress targets presents a beautiful shopping for alternative, very like we now have seen in different progress retailers in prior durations of comp softness. At current costs, traders are paying little for shares of an organization with a profitable idea that has a possibility to triple their retailer base. With continued regular execution and a medium-term honest worth estimate within the $40s, we see a possibility to earn multiples on our funding over a multiyear time horizon. For traders within the lengthy model of the story, please see our full write-up which you will discover on our web site right here.

QMCO – Once I first began Quantum Corp within the spring of 2018, I couldn’t assist however suppose it was one of many extra fascinating conditions I had seen in someday. After all, there was greater than slightly hair on it. With a market cap underneath $200M, shares had simply skilled what could possibly be described as a misplaced decade of types. Revenues and the inventory value had executed little however fall, with gross sales shriveling to ~$400M from a previous run charge of ~$1B in 2008. Although the corporate nonetheless maintained a powerful aggressive place in some essential product areas and continued to personal a stake in a helpful royalty-paying expertise consortium, it appeared of little comfort as these finish markets drifted listlessly into secular decline. Quite a few adjustments in management would observe, together with a virtually unprecedented 5 CEOs in underneath six months, in the end resulting in nasty headlines like this one: Quantum appears to undergo CEOs like a sizzling knife via butter. As a final and remaining straw, the corporate would incur accusations of impropriety within the submitting of their financials with the SEC. With the accuracy of the financials in query, the corporate would stop reporting quarterly ends in early 2018, and later that 12 months, shares could be delisted from the NYSE. The corporate would successfully go radio silent.

Indiscriminate promoting would observe, as investor views would default to the worst given the knowledge vacuum. However a better looker would present there have been some good issues creating. In Could of 2018 the corporate would rent Mike Dodson, a CFO with sturdy expertise in turnarounds and SEC investigations. Two months later, a well-regarded information storage veteran would be a part of the staff as CEO. Our contacts gave the incoming Jamie Lerner excessive marks for his in-depth product data and strategic rationale, significantly for his work in rapidly turning across the Cloud and Methods Expertise Group of Cisco by repositioning their go-to-market technique. With a formidable staff coming collectively, shareholders had purpose for slightly optimism. However there was maybe extra excellent news on the horizon as rumors started swirling that tape – the means of knowledge storage round which a lot of the firm’s merchandise are oriented – is perhaps making a comeback.

There have been loads of doubters. In spite of everything, as an affordable and clunky means of knowledge storage, tape had executed nothing however lose share to sooner and extra environment friendly choices like arduous disk drive, flash and the cloud for the final ten years. Given all of the skepticism round this potential tape renaissance, I made a decision I needed to go see for myself. That July, I went to a commerce present the Sports activities Video Group hosted in New York referred to as Sports activities Content material Administration and Storage. Anticipating to come across the kind of down-and-out feeling of nostalgia one would possibly discover at a Betamax conference, I discovered one thing totally different.

Quantum reps gave the impression to be of their aspect. They have been optimistic and speaking excitedly about upcoming next-generation merchandise on the best way. Trade gamers have been additionally speaking about new use circumstances for tape. Storage of sporting and gaming occasions was turning into a problem as tens of hundreds of high-definition clips from a number of video angles have been creating immense quantities of knowledge. On prime of that, video surveillance was much more of a priority, with some forecasts suggesting it might be accountable for as a lot as 80% of the information created on this planet by the 12 months 2025. Storing all of this information was getting costly, particularly when utilizing the current improvements which had positioned a premium on fast retrieval. However tape was low-cost. And although it nonetheless took a minute or two to entry, its ~5:1 price benefit over different mediums in a world of quickly increasing information was turning into too nice to disregard. Tape was making a comeback.

Regardless of these creating positives and a gentle stream of press releases from Quantum about new merchandise and buyer wins, so far as quarterly financials have been involved, the corporate nonetheless had little to say. Administration did exhibit they have been making progress in an 8k filed this spring. They confirmed they’d remoted the difficulty right down to recognizing solely the timing of a sure set of historic revenues, thus eliminating any unfavorable implications round historic or future money flows. However few observed. With shares depressed, draw back safety out there from the excessive margin royalty stream and finish markets doubtlessly turning of their favor, we initiated a small place this summer season.

This August the corporate would lastly converse. As anticipated, their financials required little in the best way of a restatement of something of consequence. As an alternative, what they confirmed was that new administration had made a substantial amount of progress with the corporate whereas away from the highlight. The staff had modified the gross sales rep compensation scheme to reward earnings over gross sales and equally applied a streamlined go-to-market technique targeted on solely its strongest product choices. The consequence: in a 12 months and a half, administration had reduce some $70M of annualized prices and pushed gross margins 400 bps increased. The EBITDA run charge had practically doubled to ~$51M from the prior 12 months, and administration would focus on expectations for high-single-digit annual income progress from the secular beneficial properties of a rising tape market going ahead. The outlook was enhancing.

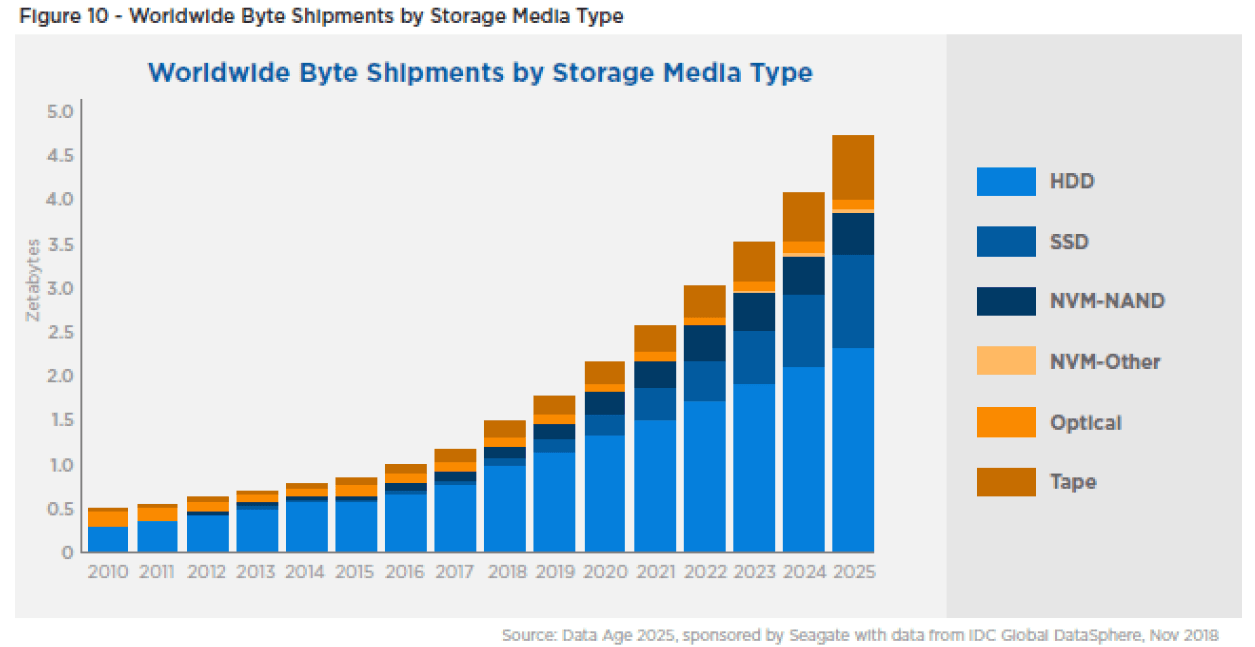

Apparently, this income outlook contemplates little in the best way of latest enterprise from fulfilling the information wants of the hyperscalers. These are the enormous firms like Google, Amazon, Microsoft, Fb and Apple who’re storing the world’s information and accordingly have massively increasing information storage wants of their very own because the chart on the fitting from IDC exhibits. Although any contract wins right here shall be episodic in nature and include lengthy promoting cycles, they are often materials, doubtlessly to the tune of $30M or extra in annual revenues. There are in fact no ensures Quantum will land any of this enterprise. However because of the corporate’s legacy place within the trade, they give the impression of being properly positioned. They have already got an current relationship with one of many largest hyperscalers, and a minimum of in the interim, look to be preventing primarily with only one different participant to win the remainder.

Although Silicon Valley character Gavin Belson’s views of knowledge shortages and information rationing from an impending datageddon are in fact a bit hyperbolic, the purpose, because the IDC forecast suggests, is identical: the world will quickly be awash in information and it’s going to have be saved someplace. At 8x this 12 months’s FY20 EBITDA, little progress or additional enchancment in operations seems to be priced in, regardless of an outlook that seems to be enhancing. Within the brief time period, we see coming catalysts with an up-listing again onto the Nasdaq on the horizon, a rising royalty stream and new buyer wins. Over the medium to long run, we consider Quantum is poised to profit from the secular pattern of rising information storage wants and see a possibility to earn multiples on our funding over a a number of 12 months time horizon with continued regular execution.

2019 Outlook

Our home financial system seems to proceed to run at two speeds. Development in lots of industrial companies is sluggish or stalling out. Whereas an enter for the speed of progress of the financial system at giant, at ~11% of exercise in the present day, the manufacturing financial system doesn’t carry the identical ramifications for the remainder of the financial system it as soon as did. However, most areas of the financial system reliant on client spending proceed to indicate resilience. A number of rate of interest delicate areas of the financial system appear to be perking up, as information collection like current dwelling gross sales and furnishings gross sales at the moment are rising once more after a pair quarters of weak spot.

In opposition to this uneven backdrop, markets at the moment are usually flat with their ranges from a 12 months in the past, with each the extent of earnings and the a number of paid for them largely static over this era. Present indications counsel we proceed to flirt with one other transient earnings recession, although its worst results could also be transferring to the rearview mirror in the interim.

Whatever the market’s gyrations within the brief time period, I consider our eclectic portfolio seems to supply better worth and seems set to carry out properly on this atmosphere. Although our holdings will assuredly be influenced by the market route within the brief time period, within the medium to long run, our efficiency shall be pushed by the enterprise outcomes of those particular firms and the unfolding catalysts that lie forward.

Conclusion

In closing, whereas I do know our method is not going to yield outperformance each quarter, I proceed to consider it will likely be properly value our whereas over the lengthy haul. Maybe extra importantly, given the overwhelming majority of our investable belongings are invested alongside yours, we might by no means ask traders to imagine dangers we ourselves is not going to.

Thanks in your continued assist as we work to develop our capital collectively. As all the time, we’re completely happy to debate our funding outlook with you at your comfort. Please attain out any time.

Finest regards,

Mitchell Scott, CFA

Portfolio Supervisor

All market and firm information is sourced from Factset and firm filings and is present as of 9/31/19.

CEF makes use of the S&P 500, Russell 2000, a customized Blended Small/Giant Benchmark and the Barclays Hedged Lengthy/Quick indices as its major benchmarks. The S&P 500 and Russell 2000 are widespread giant and small cap US equities-based indices. The customized Blended Small/Giant Benchmark is supplied to seize a bigger proportion of small cap efficiency versus giant cap efficiency (at a three:1 ratio) as a result of equally excessive proportion of small caps discovered on the Good Companies Focus Checklist in addition to the technique’s basic choice of getting an funding combine extra closely weighted in direction of funding in small caps. The Barclays Hedged Lengthy/Quick index (an index of equities-based hedge funds) serves as an applicable benchmark over the long-term given the index has an identical long-term objective of capital appreciation via equities investing.

CEF Internet Returns are hypothetical outcomes calculated from precise gross ends in a fashion according to the 1% administration price and 18% efficiency price provided to shoppers.

APPENDIX

CEF GOALS, PHILOSOPHY, APPROACH AND ALIGNMENT

GOALS – We search to generate market-beating returns over any rolling multiyear funding horizon whereas minimizing the danger of everlasting impairment of capital. Moreover, we search to speak with our traders in a clear and simple method and ask solely that they settle for funding dangers that we ourselves are prepared to take. Given the vast majority of our investable capital is invested alongside theirs, we make investments our restricted companions’ capital as if it have been our personal, as a result of it’s.

PHILOSOPHY – We method investing in public equities as an opportunistic businessman would. We spend most of our time learning companies and constructing circles of competence in areas prone to provide engaging funding prospects and put money into solely our most compelling alternatives. We view danger primarily because the probability of a everlasting impairment of capital and pursue a fastidiously balanced willingness to commerce some short-term portfolio fluctuations for the chance to earn increased returns over the long-term. We give attention to rising, comprehensible companies and search to purchase them at a considerable low cost to our estimate of their intrinsic worth. After we discover them buying and selling at engaging costs, we regularly act in measurement and weight our greatest concepts accordingly. And all issues being equal, we desire to dedicate extra of our efforts to small shares the place we consider better value/informational inefficiencies can usually be discovered.

APPROACH – We make investments through a long-bias hedge fund construction and focus our lengthy investments in our greatest 10 to 15 concepts. Our work begins with a two or three-year outlook, and we solely pursue investments we consider are prone to provide us an affordable probability to generate an annualized return of 20% or higher. Whereas we pursue long-term oriented investments and search to compound capital in a tax environment friendly method, we readily acknowledge the often-turbulent markets don’t all the time match neatly into this framework and know some buying and selling exercise is bound to observe because of this. Within the brief e book, we search to generate absolute earnings in just a few shares the place we now have uncovered an organization getting into monetary duress or an excessively optimistic valuation the place we really feel their earnings outlook is prone to worsen materially. We may also use trade or market particular ETFs to mitigate market danger and can look to make use of choices and different opportunistic hedges when situations seem favorable.

ALIGNMENT – We consider applicable alignment of pursuits is the bedrock upon which all profitable partnerships are constructed. Our major technique of guaranteeing correct incentive alignment is thru vital co-investment of our private wealth alongside our restricted companions. Secondarily, we provide an investor pleasant price construction. We cost a modest administration price to assist funding operations and cost an annual incentive price on new earnings solely. Lastly, commensurate with our price construction which is deliberately structured such that almost all of fund earnings shall be earned provided that we generate compelling funding outcomes, we decide to working the fund as a boutique store with a restricted asset measurement. As a lot of our greatest investments usually come from small shares, we consider it is very important protect our means to take concentrated positions in our greatest concepts. Our measurement and construction guarantee we’re incentivized to generate compelling returns, not collect belongings.

Consider it this fashion. On the one hand, we’re incentivized to generate the very best funding outcomes potential. However, we’re unwilling to put money into a approach we really feel is prone to end in a significant lack of our personal funding capital. What extra might one need from an funding supervisor?

source https://jobsearchtips.net/alternative-equities-fund-3q19-investor-letter/

No comments:

Post a Comment