Forge First Asset Administration commentary for the month ended November 30, 2019.

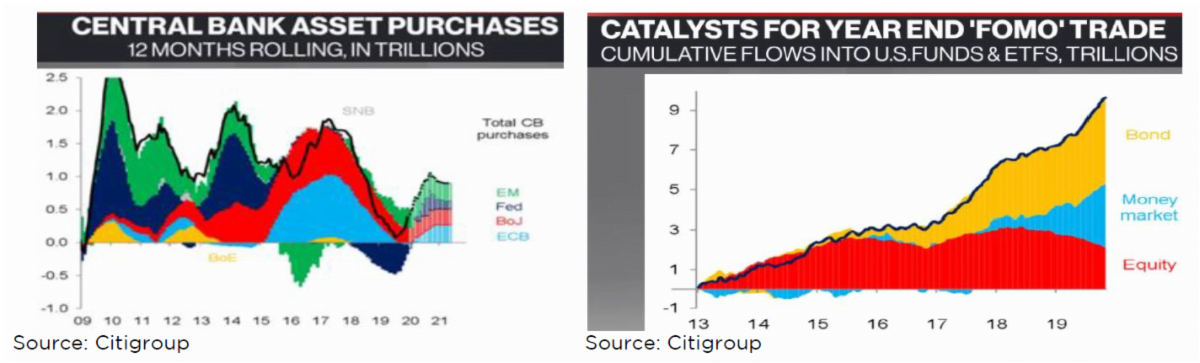

The angle of traders in the direction of equities was buoyed final month by optimism China U.S. commerce deal would get achieved, perception that the speed of change in international financial exercise had bottomed and information that the Federal Reserve was rising its steadiness sheet once more. Whether or not one calls it QE or not, in becoming a member of the Financial institution of Japan and the ECB, the graph on the beneath left reveals the clear reversal from the steadiness sheet tightening of late final yr. The truth is the dashed line of ahead estimates on the appropriate aspect of the graph reveals this newest central financial institution social gathering is simply getting began. In consequence, after having bought equities to purchase cash market and bond funds in the course of the previous couple of years (please see the graph on the beneath proper), FOMO (‘fear of missing out’) catalyzed traders to begin chasing shares. This renewed shopping for drove the sturdy November for shares, one which included 11 recent all-time highs for the S&P 500.

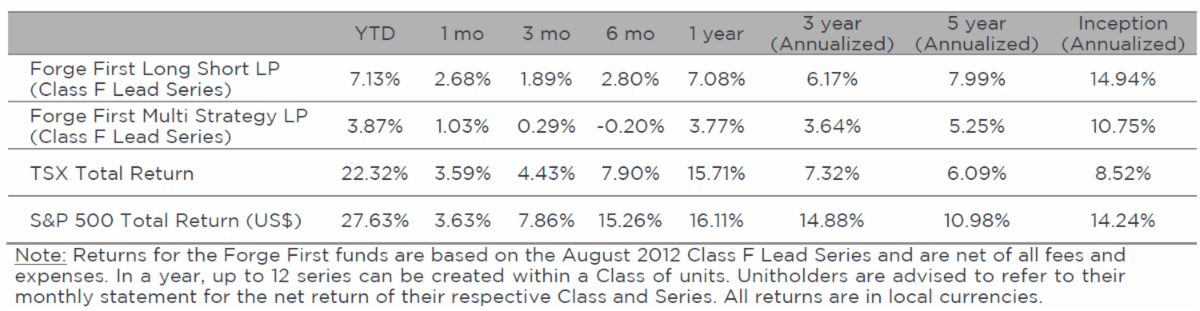

Every of the 2 funds at Forge First joined this social gathering with sturdy positive aspects for the month, with every fund exiting November at an all-time excessive. The supply of the earnings was widespread though our lengthy place in Canadian oil sands corporations and quick shares in U.S. power corporations topped the charts of sector efficiency. First mentioned in our Might 2019 commentary the Canadian oil corporations held in our portfolios are minting money at present oil costs whereas a lot of the U.S. E&P universe is struggling.

For instance, high 10 holding Canadian Pure Assets Ltd. (CNQ.CA) generated $1.9B of free money circulate from the 1.1M BOE/day it produced throughout Q3. In distinction, a universe of U.S. mid-cap corporations that collectively produced eight.5M BOE/day throughout the identical time-frame generated $1B of free money circulate. Given the mixture of enhancing close to time period egress for Canadian oil (Line three, crude by rail) and our forecast that WTI oil costs will stay within the $52-$62 value vary in the course of the subsequent couple of quarters, we count on this divergence in efficiency to proceed.

Different key contributors to November’s efficiency had been core holdings Goeasy Ltd. (GSY.CA), Parkland Gas Corp. (PKI.CA) and Microsoft Corp. (MSFT.US). The one dropping sectors had been ETFs, predictably as these funds are used as beta hedges to our portfolios, and supplies, as the value of gold fell three% on the month.

Assuming President Trump doesn’t upset the commerce cart, we’d count on FOMO to allow this Santa Claus rally to proceed within the quick time period. We should admit the common consensus of this constructive view in the direction of equities offers us pause although the final calendar month of the yr has traditionally been a optimistic one for shares 72.5% of the time.

Nevertheless, in the long run we’re comfy with our internet lengthy frequent fairness positioning (49.eight% within the Lengthy Quick LP and 24.2% within the Multi Technique LP) as a result of 1) we’ve rolled our index places to greater strikes, 2) maintain listed possibility positions on many particular person positions, and three) we maintain a diversified quick ebook, as is a part of our investing rulebook.

Wanting forward into 2020, whereas our outlook commentary can be launched in early January, it’s robust to see how subsequent yr can get higher than 2019 for the broader fairness indices. Based on Morgan Stanley, regardless of optimistic income progress, earnings for the S&P 500 have usually not grown for three consecutive quarters. Additional, earnings for small and mid-cap corporations are down near 10% from their peak whereas the payout ratio for the S&P 500 exceeds 100%. With valuation growth having accounted for roughly 90% of the rise in inventory costs this yr, the PE ratio on 2020 EPS now exceeds 18.5X.

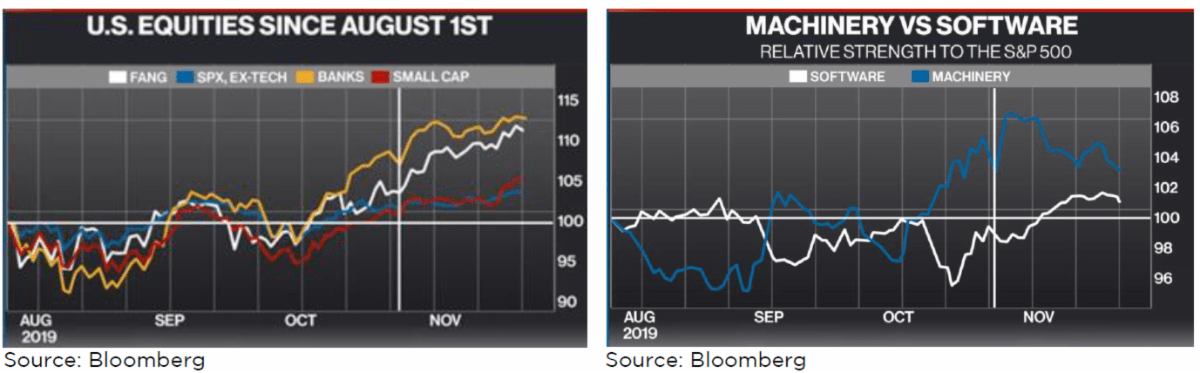

Consequently, whereas not proudly owning sufficient shares was the ‘pain trade’ for 2019, we imagine sector rotation would be the ache commerce for 2020. Every of the graphs of U.S. shares proven beneath begins on August 1st, the inception of this newest rally, with the white vertical line marking the beginning of November. Usually talking, this four-month transfer in shares that we’ve now skilled has usually exhibited a price/cyclical versus progress/momentum bias. Nevertheless, the graph on the left reveals that banks (orange line) and the broader ‘FANG’ index (white) have outperformed small caps (purple) and the non-tech elements of the S&P 500 (blue), particularly throughout November. This little bit of a stall within the progress to worth commerce is especially apparent from the graph on the appropriate, the extremely cyclical equipment index (blue line) versus epitome of progress and momentum, the software program index (white line).

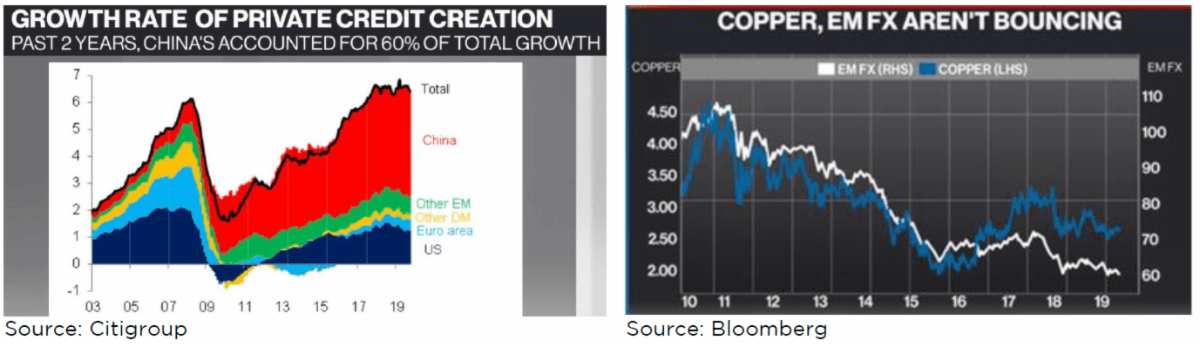

At this juncture there are causes to be each optimistic and pessimistic in the direction of the market’s present enthusiasm that international progress will speed up. On the detrimental aspect of the ledger, the graph on the beneath left highlights that China has accounted for 60% of worldwide non-public credit score progress in the course of the previous two years. Neither the present trajectory of falling progress in industrial earnings nor Beijing’s admission of concern in the direction of the prevailing monetary leverage of their financial system is conducive to a continuation of above common credit score creation. In the meantime, the graph on the beneath proper reveals that two conventional main indicators of enhancing progress (albeit extra related for rising vs developed markets) stay dormant.

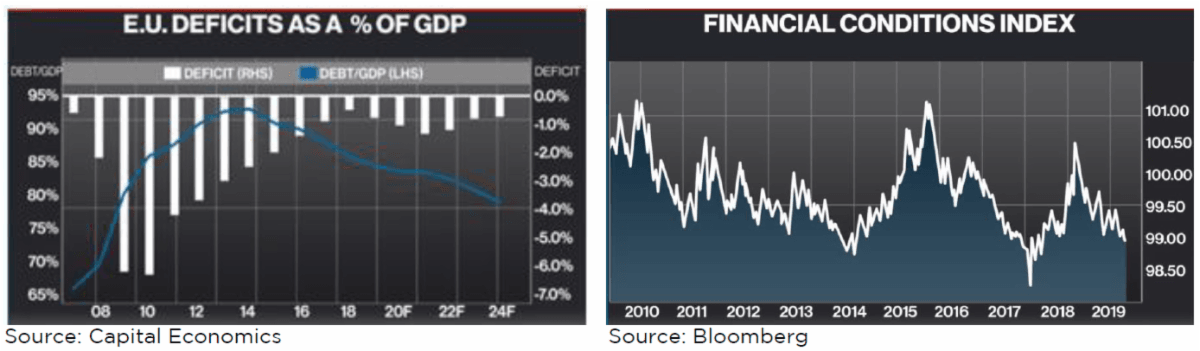

On the identical time, it’s fairly clear that the massive three central banks intend to stay extremely accommodative (low charges, rising steadiness sheets) till nicely into 2021. That’s simply one of many the reason why the Goldman Sachs monetary circumstances index proven on the beneath proper is as unfastened as it’s proper now. As well as, whereas we stay circumspect that we’ll see substantive fiscal stimulus from the EU in a well timed style, the graph on the beneath left illustrates that the continent positively has the monetary wherewithal to maneuver forward with a sizeable program.

If progress does reaccelerate, we’d count on to see a continued shift away from progress in the direction of worth and extra cyclical companies. Nevertheless, with ‘no new China’ to drive a commodities increase, this fairness shift can be extra selective than that of earlier upcycles. On the identical time, whereas we don’t know the particular numbers, the implicit shift within the circulate of funds may very well be very highly effective for successful sub-sectors.

Macro cap tech shares are universally owned. If 10% of the holders of those shares bought 5% of their positions in favour of shopping for cyclical shares, this quantity of capital might dwarf the present market cap of the successful cyclicals with out shifting fairness indices all that a lot. In distinction, if progress doesn’t reaccelerate by Spring time, and by then fairness markets begin becoming concerned a couple of Warren White Home, the rotation that’s already occurred might reverse, once more with little motion within the broader averages since such a ‘risk off’ commerce would see the closely weighted macro cap shares bought throughout the board.

The opposite merchandise that can play a key position in both situation is the U.S. greenback. Reaccelerating international progress would lastly push the Yankee buck decrease whereas stall velocity or worse might push the ‘DXY’ index to par. A guess on the greenback is a guess on which financial situation you count on and therefore how an investor doubtless desires to be positioned.

At Forge First, we’re not going to ‘make a bet’ both manner. For instance, as mentioned in our final market commentary throughout mid-October, we made tactical shifts to our portfolios. These strikes elevated our publicity to extra cyclical corporations, with out forsaking both of our free money circulate self-discipline nor considerably altering our drawdown potential.

One new title that match this profile was Patrick Industries Inc. (PATK.US), a components producer for manufactured housing and RVs, an organization with enhancing fundamentals and a double digit free money circulate yield. As for not materially altering our publicity to a big drawdown, we shifted our index put unfold publicity to proudly owning straight places. Additionally, we changed a number of single inventory shorts with broader market hedges through ETFs.

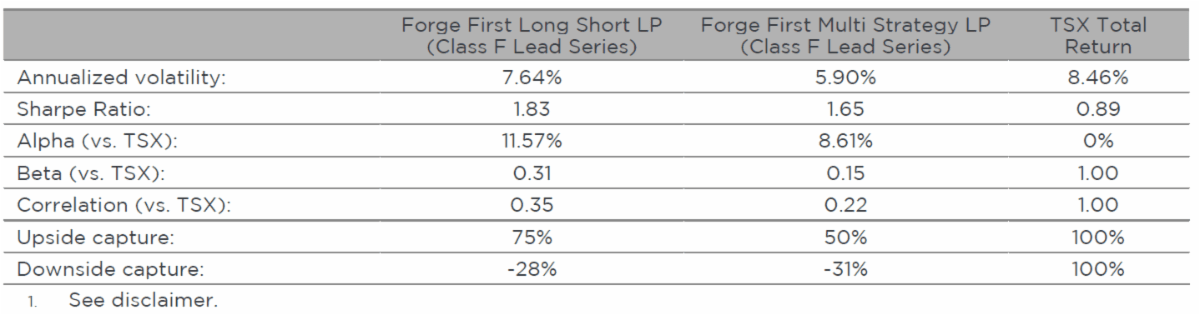

Consequently, we’re very comfy that the present positioning of our portfolios provides strong cyclical upside but glorious safety of the draw back. After all, that’s what different funding funds are imagined to be all about, and it’s why our funds have a strong risk-adjusted internet return profile since their inception greater than seven years in the past.

As at all times, thanks to your consideration. Please go to our web site at www.forgefirst.com for data on our funds. Ought to you might have any questions, please contact us.

Most of all of the group at Forge First wish to want you and your family members a wholesome and glad vacation season.

Thanks,

Daniel Lloyd

Portfolio Supervisor

Andrew McCreath, CFA

President and CEO

Get The Full Warren Buffett Sequence in PDF

Get the whole 10-part collection on Warren Buffett in PDF. Put it aside to your desktop, learn it in your pill, or electronic mail to your colleagues

Q3 2019 hedge fund letters, conferences and extra

source https://jobsearchtips.net/forge-first-lengthy-canadian-oil-sands-quick-us-power/

No comments:

Post a Comment