The Boeing Company (BA) will be publishing its results on Jan. 29. In this report, we will have a look at analyst expectations, earnings as projected by our model and what risks there are surrounding Boeing’s share price.

Source: Reuters

Before we start…

We’d like to emphasize that these earnings estimates are in no way intended to shock or take a contrary stance as some readers seem to be expecting each quarter. Sometimes when the EPS indications are in line with what analysts expect, we’re being asked why we even bothered writing a report with our expectations. The reason is that most of you will go and look at analyst estimates and say “Hey, this is the consensus.”

If the reported figures are below consensus, then earnings were disappointing. If it’s above the consensus, then earnings were terrific. That’s all nice, but the truth is that each analyst makes assumptions that you often do not see.

In this report, we’re showing you our assumptions and calculations, and that’s where the AeroAnalysis report differs from just looking up the consensus. Sometimes, our findings match the consensus, but that does not mean we should not write about that. There are a lot of elements that affect the reported figures, and in these reports, we’re showing how certain moving elements affect estimated earnings.

This piece does not constitute any buying or selling recommendation based on any differential between our estimate and realized figures. Far more importantly, we’d like our readers to see in detail how we got to the core earnings figures as an informational piece.

With the Boeing Global Services unit being added in 2017, the number of possible combinations of margins and revenues adds up significantly. So, while we do like to provide several scenarios, we will limit ourselves here to nine at most, and that already represents a lot of combinations. What you should pay special attention to is the impact that a 0.5-point margin difference has on the earnings per share. This is partly caused by the revenue streams multiplied by a margin that already cause quite a big difference, and this is further amplified by the share count coming down. Over the past four years, the share count has come down by more than 20%. This obviously drives value to shareholders, but it also means that any earnings beat or miss looks much larger than it previously would have.

One thing investors should be aware of is that the revenue recognition for services and military aircraft derived from commercial aircraft is hard to predict as revenues from services occur as these services activities are performed. For Services, there should be a nice layering of revenues. However, for military aircraft, the costs are being recognized during the production process it seems, and at this stage, we don’t know a single thing about revenue distribution for military deliveries.

In 2019, Boeing started attributing costs and revenues from military aircraft such as the Boeing KC-46A and Boeing P-8A that are derived from commercial base models to the military segment. Results from 2018 have been restated accordingly but still do provide a renewed challenge for us to estimate performance across all core businesses of the company, since Boeing Global Services reported figures now also include revenues from the KLX Aerospace Solutions Group that Boeing acquired last year.

If these changes did not provide for a big enough challenge to estimate the revenues and earnings, the current problems with the Boeing 737 MAX do provide a lot of uncertainty with respect to earnings. If our assumptions drastically differ from Boeing’s execution during the quarter, our estimates might significantly differ from realized results, and we urge readers to take this into account when reading the report.

Revenues

Revenues are quite difficult to pin down. Theoretically, for the Defense & Space unit, we can look at sales contracts to determine the values. The unknown, however, is when deliveries occur and how much of the revenue is being recognized upon delivery. So, while the contracts and values are available, it’s hard – and we think almost undoable – to connect the deliveries occurring in a certain quarter to specific contracts, values and revenues. To come up with revenues for the Defense, Space & Security unit, a quarterly distribution of the segment revenue is used.

For commercial aircraft, a similar thing holds. Contracts for commercial aircraft are not publicly available and the pricing varies from customer to customer. With more than 75 deliveries targeted per month on average when delivery profiles aren’t depressed, it’s also difficult to treat each delivery as a delivery with unique pricing and discounts. Instead, average pricing is used to estimate revenues of the Boeing Commercial Airplanes unit.

At the start of the second half of 2017, Boeing elevated its services unit to operate on the same level as the Defense and Commercial Airplanes units. Decoupling this services unit from BCA and BDS emphasizes the importance and growth prospect of the Global Services unit and also should allow the business to operate more efficiently. What we like about this newly formed unit is that its revenues are more or less constant throughout the year with solid margins. With Boeing’s renewed focus in the after-sales market, there’s a lot of room for growth in this particular area.

Source: Seeking Alpha PREMIUM

For the fourth quarter, the consensus among analysts for revenues is $21.02B.

For the Commercial Airplanes department, deliveries have decreased sharply year over year, driven by the delivery stop for the Boeing 737 MAX. As a result, based on our internal modeling, we’re expecting revenues of roughly $10.15B, signaling a 40% decline compared to Boeing’s restated revenues for the third quarter of 2018. This reduction in revenues really shows the importance of Boeing’s single aisle aircraft business. What also should be considered are possible additions to the liabilities which I expect to be in a positive scenario to be in the $6B-$6.6B range which is expensed against revenues as well as Boeing Commercial Airplanes earnings bringing the revenues estimate for Boeing Commercial Airplanes to $3.56B.

Revenues from the Defense, Space & Security and Global Services segment have proven to be more difficult to estimate since it’s somewhat harder to estimate the revenues for the Network, Space & Systems and the Global Services & Support segment. Using the distribution of revenues throughout the year, we’re expecting revenues between $6.2B and $7.3B.

For the Global Services unit, we are expecting revenues of $4.68-5.68B.

In aggregate, we expect revenues to come in between $14.5B and $15.6B in an optimistic scenario. That’s quite a bit lower than the $21B consensus but can be explained by the consensus not having the liabilities update included. From previous quarters, we do know that there have been times that we have been too conservative in our estimates. We could try and factor this in, but it would defeat the purpose of the calculation models. Therefore, we’ve chosen to present the numbers as is without correctors. Correctors are nice, but with a business such as Boeing’s, even the correctors do not remain stable, so the implementation of a corrector would require a corrector-predictor, and we think that’s something where we shouldn’t go. Our estimate is $800 million lower than the consensus.

Earnings

Estimating revenues already is quite difficult. Estimating earnings is even more challenging. In the case of charges, the earnings figures will be far off in comparison to the estimates if they aren’t accounted for beforehand. Presently, we expect that Boeing is actually missing their Q1 return-to-service window, which might cause additional charges. For investors, it’s good to keep in mind that each $1B directly charged to the company’s earnings results in a $1.77 headwind in pre-tax earnings per share.

It’s hard to say what Boeing’s liabilities update will look like. Currently I’m expecting that it will be $6.6B in the best case scenario, $8.6B in our mid-point scenario and $11.5B in our worst-case scenario, based on current provided schedule (which is at risk of slipping given Boeing’s history with being able to provide realistic planning).

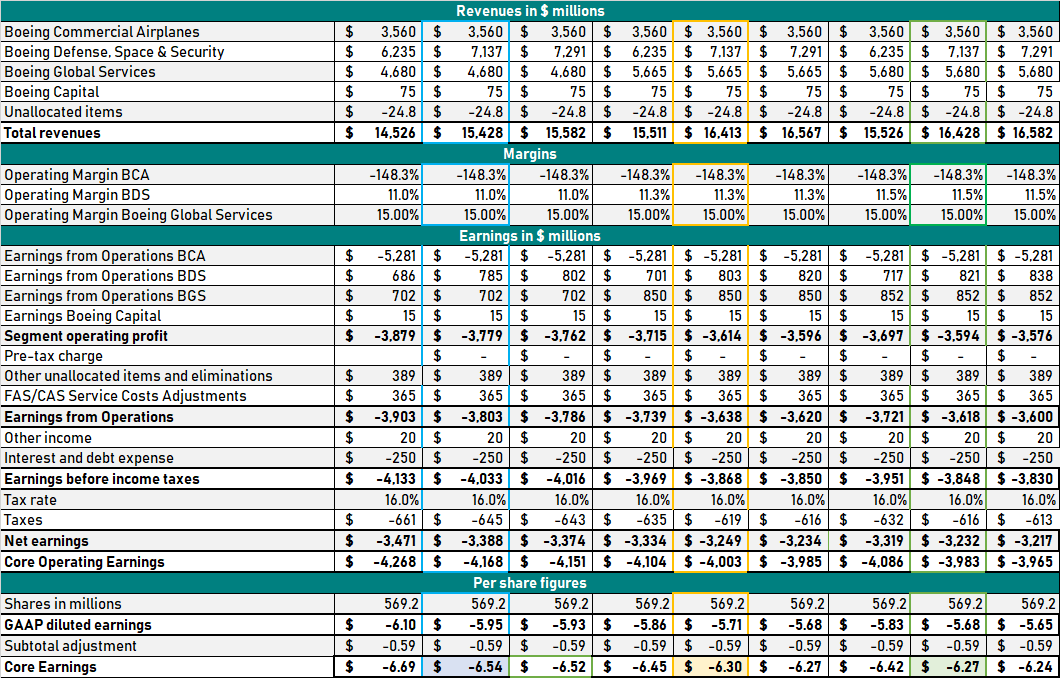

Earnings Scenario 1

Table 1: Earnings estimate Boeing Q4 (Source: AeroAnalysis)

What you see is quite a range of core earnings estimates, and that requires some explanation. First of all, the reason to supply a range rather than one revenue figure or margins is to show what a half percent here or there does to earnings, and that’s quite sensitive since a 0.5 point difference in margins in Boeing Commercial Airplanes leads to a $0.11 change in core earnings per share and ~$0.20 per share if there’s a change of 0.5 points on all segments. Secondly, it might give an idea on how other analysts came to their core earnings estimates.

With Boeing consisting of three main segments, the number of possible margin and revenue couples increases as well. We are certainly not looking at all combinations, since there are many and too many to analyze in a useful way. We have three revenue estimates, and each of these is coupled to three margin groups, so we end up with nine ways to drill down to core earnings per share.

The average estimate leads to an EPS estimate of -$7.25 per share. The consensus estimate is $2.10, but this likely does not include Boeing’s update to the 737 MAX liabilities. While -$7.25 in earnings does look horrible, I am also expecting around $3.5B in additional costs that could be put in block costs for the Boeing 737 program.

For Boeing Commercial Airplanes, we’re expecting margins including the liabilities update around -150% for the fourth quarter while we expect margins of 11.0-11.5% for Boeing, Defense, Space & Security. For Boeing’s services unit, BGS, we’re expecting margins of 15%. Boeing had previously guided for an effective tax rate of around 16% for the full year.

Possibly, we will see Boeing “benefiting” from a lower effective tax rate which could increase earnings, but earnings are unlikely to be pretty… the expected increase in liabilities is simply too big for that.

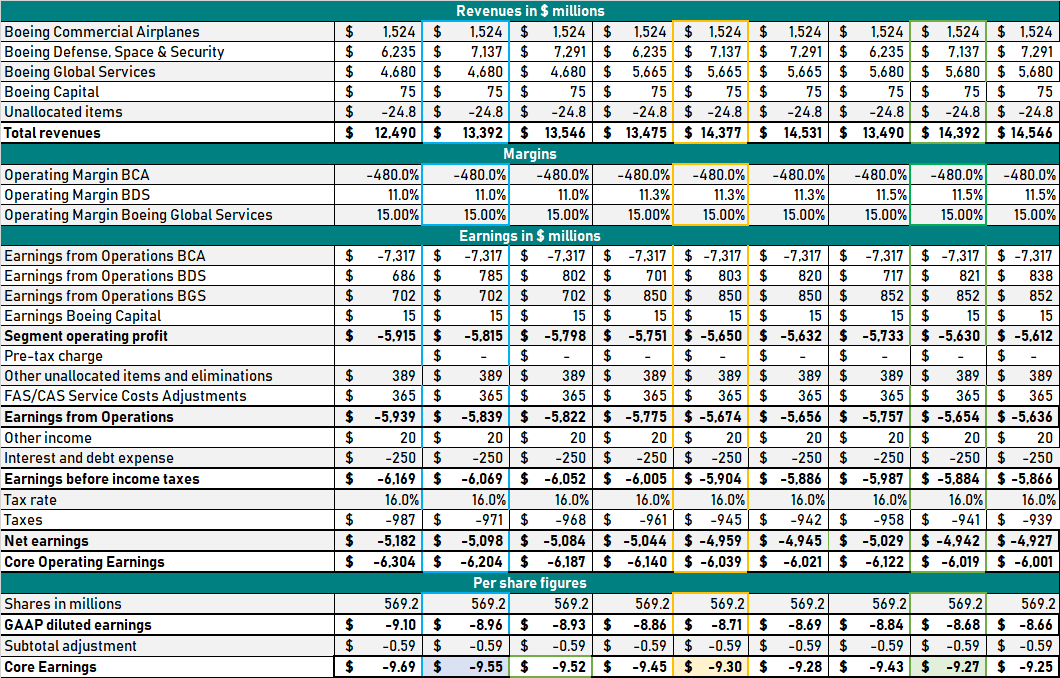

Earnings Scenario 2

In the second scenario the revenues come down to $12.5B-$14.5B as liabilities are subtracted from profits as well as revenues putting the EPS in the negative $9.25-$9.70 range.

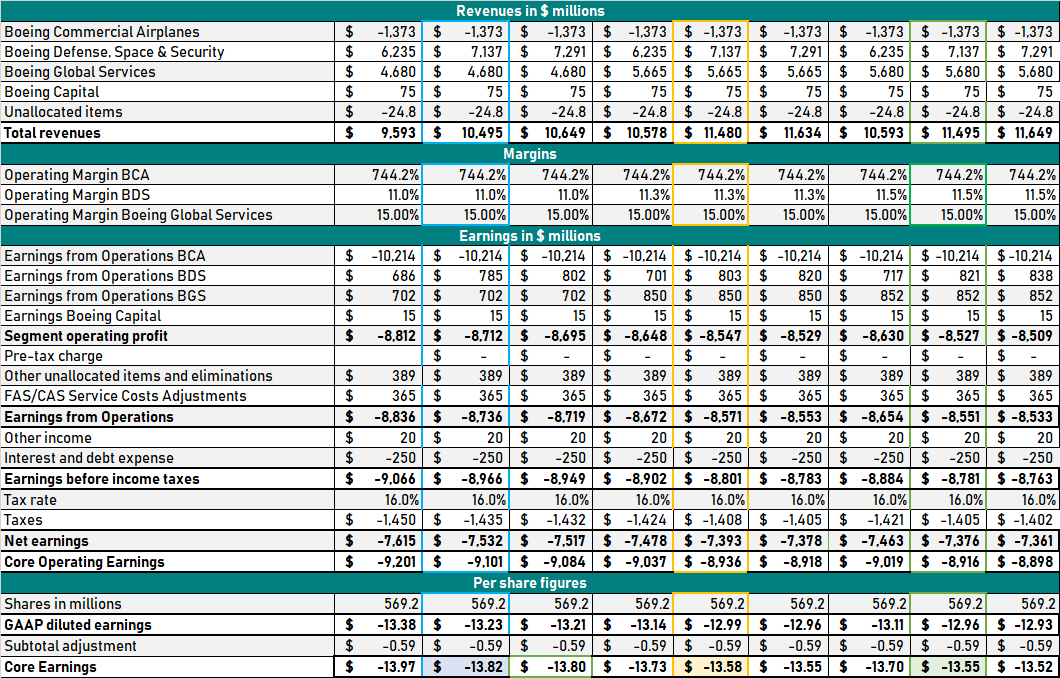

Earnings Scenario 3

Doing the same for the “worst-case” scenario, which would put liabilities update at $11.5B, we would get to a revenue $9.6B-$11.65B with losses of $13.50-$14.00 per share.

Cash flow

Important for Boeing shareholders will be the cash flow profile, which is even harder to estimate than earnings and revenues. At this point, we’re expecting a dent in Boeing’s free cash flow profile due to the delivery stop on the Boeing 737 MAX program. The stop could shave off $2-3B in cash flows, but it remains to be seen whether Boeing has been able to quickly adapt its receipts and expenditures profile to minimize the in-quarter impact.

Risks

Source: CNBC

A year ago, very few would have expected that the Boeing 737 MAX would be considered a risk, though admittedly I have seen some readers making the right call on the MAX crisis in a well-reasoned way. The truth is that, going from Q3 2018 to Q4 2019, the world looks a whole lot different to Boeing, airlines and the traveling public. Days after Boeing reported Q3 2018 results, the first crash with the Boeing 737 MAX occurred. It would be the start of a revelation of what went wrong in the design and certification process of the Boeing 737 MAX. At this stage, the Boeing 737 MAX is a risk to Boeing’s financial performance. As long as the delivery stop lasts and the aircraft remains grounded, Boeing is facing compensation requests from customers as well as lower revenues that stretch beyond the charge Boeing already has recognized.

Currently being a Boeing shareholder is a big risk. Whereas we normally are talking about costs in the millions or Boeing missing revenues by a million here or there and a cent here and there on earnings per share, we are now talking billions in added costs. If you have $6.5B in added costs, that’s roughly $11.50 in costs per share. Those are huge costs. At present, you should consider Boeing a busted growth story.

Conclusion

We’re expecting a disastrous quarter with significant pressure on Boeing’s earnings. If my calculations are anywhere near correct there will be low revenues, low earnings, increased liabilities on the balance sheet, increases in inventory and increases in debt and interest payments. I expect that wherever you will look you will be able to see that Boeing emaciated itself while seemingly booking extremely little progress in marching the timeline since November 2019.

The only way in which Boeing’s earnings could be looking less horrible is if part of future compensation is not re-corderd during the quarter, but expensed as various forms of compensations are being rendered although I wouldn’t see why Boeing would opt for that construction as it would go against the way the company has already recognized MAX liabilities and would erode future revenues and margins.

Let me know your expectations for the Boeing 737 MAX in the comment section.

*Join The Aerospace Forum today and get a 15% discount*

The Aerospace Forum is the most subscribed-to service focusing on investments in the aerospace sphere, but we also share our holdings and trades outside of the aerospace industry. As a member, you will receive high-grade analysis to gain better understanding of the industry and make more rewarding investment decisions.

Disclosure: I am/we are long BA, EADSF. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

%

source https://jobsearchtips.net/boeing-737-max-crisis-triggers-multi-billion-dollar-charge/

No comments:

Post a Comment