Last October, Tesla (TSLA) announced a big Q3 earnings beat. While the electric vehicle pioneer’s adjusted EPS of $1.86 was down from $2.90 a year earlier (when the company was benefiting from an unusually rich sales mix), the analyst consensus had called for a quarterly loss.

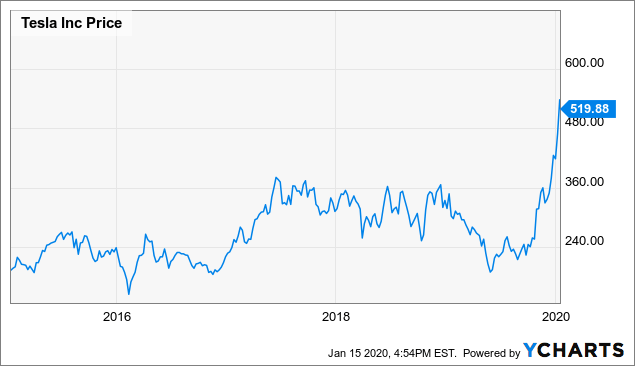

This solid result helped snap Tesla stock out of a multiyear funk. The on-time opening of Tesla’s Gigafactory Shanghai, strong Q4 production and delivery figures, and growing excitement about the upcoming Model Y crossover added fuel to the fire. As a result, the stock has more than doubled in the last three months, surging to a new all-time high well above $500.

Data by YCharts

Data by YChartsIndeed, there are several big growth opportunities around the corner for Tesla. That said, these opportunities are not as much of a slam dunk as bulls seem to assume. As a result, Tesla stock does not look attractive at its current valuation.

The Model Y is coming soon

The biggest growth catalyst coming for Tesla is the introduction of the Model Y midsize crossover later this year. In the U.S., China, and many other markets around the world, consumer preferences have shifted decisively in favor of crossovers rather than sedans. As such, it’s impressive that Tesla has had so much success with a vehicle lineup tilted sharply towards sedans.

Last year, Elon Musk predicted that demand for the Model Y could be 50-100% higher than for the Model 3, due to crossover’s popularity with consumers. That seems like a reasonable estimate.

However, it’s not clear that 2019 Model 3 sales are the right baseline to measure from. Many Model 3 customers have bought the car because they wanted an affordable Tesla, not necessarily because they prefer sedans to crossovers. As a result, as Model Y availability grows, Tesla’s new crossover is likely to cannibalize demand for the Model 3.

This wouldn’t be unprecedented. Deliveries of the pricey Model S and Model X fell about 33% year over year in 2019 as Model 3 output surged. Furthermore, there are signs that Model 3 demand in the U.S. has already flattened out, even before the Model Y has become available. (The Model 3 was the best-selling car in California in the second half of 2018 but fell to third place for the first nine months of 2019 as a whole.)

(The Model Y is likely to cannibalize Model 3 demand. Image source: Tesla.)

Adding to the pressure on Tesla, a host of legacy automakers and new start-ups are beginning to introduce EVs and plug-in hybrids at a rapid pace in the U.S. In late 2018, Automotive News reported that there were nearly 100 new electrified models due to arrive by 2022. If anything, that number has grown. Moreover, most of these automakers will continue to benefit from federal tax credits of up to $7,500 per vehicle for several years: credits that have fully phased out for Tesla purchases.

I still expect Tesla’s sales in the U.S. to grow over the next two years as Model Y production ramps up. But it’s unlikely that the company’s total deliveries in the U.S. will double, let alone triple.

Made-in-China Model 3s

The recent launch of Model 3 production in China could also be a catalyst for faster growth. For one thing, the opening of Gigafactory Shanghai, which can produce at least 3,000 vehicles per week, has significantly increased Tesla’s global production capacity.

Moreover, by moving to local production in China, the company can avoid stiff tariffs on vehicle imports. This will allow it to price its vehicles more competitively, bolstering demand. For example, Tesla initially priced the made-in-China Standard Range Plus model at 13% less than it had been charging for a comparable U.S.-made Model 3. It recently cut the price further, and is contemplating further price reductions later this year as it localizes production of more components, according to Bloomberg.

That said, Tesla is opening Gigafactory Shanghai at an inauspicious time. After years of growth powered by generous government incentives, EV sales fell in China last year, contracting along with the broader auto market. A roughly 50% cut to government subsidies for EVs and plug-in hybrids last summer contributed to this downturn in a big way.

For the moment, China is holding off on previous plans to phase out subsidies entirely. The Model 3 qualifies for a subsidy of 24,750 yuan and is exempt from the 10% purchase tax that applies to non-electric vehicles. But if these subsidies/tax breaks are removed in the next few years, it will put further pressure on EV sales and offset much of the savings to consumers from localizing Tesla production.

(Tesla recently began Model 3 production in China. Image source: Tesla.)

Additionally, even with the subsidies and recent price reduction, the starting price for a made-in-China Model 3 is over $43,000. While there are 4.4 million millionaires in China, this price tag still puts the Model 3 out of reach for the vast majority of Chinese consumers.

Lower prices for the Model 3 and introduction of the Model Y should allow Tesla to fill out its current production capacity of 150,000 units per year in Shanghai and possibly grow beyond that. However, unless the company can bring prices significantly lower over the next few years, it may struggle to sell 500,000 vehicles annually in China. (That’s the plant’s theoretical production capacity, which could be reached following a second phase of construction.)

Other international growth opportunities

Globally, Model 3 deliveries surged more than 40% year over year in the second half of 2019, despite evidence that growth in the U.S. (Tesla’s largest market by far) had slowed or even stalled entirely. That points to growing adoption in international markets, aside from just China.

This isn’t surprising, as Tesla only began Model 3 deliveries in Europe in February 2019. Deliveries began even later in the U.K. The introduction of the Model Y will provide a further sales lift, as in other markets. Tesla’s decision to build a new Gigafactory in Berlin (announced in November) shows that it is bullish about its future in Europe.

A broader product lineup should help the company continue to grow in Europe in 2020 and 2021. Nevertheless, there’s no reason to believe the market will behave differently than the U.S., where demand for Tesla’s three in-production models appears to have flattened out.

(Image source: Tesla)

For example, Tesla’s two biggest markets in Europe in 2019 were Norway and the Netherlands. However, sales in the Netherlands surged late in the year ahead of the expiration of EV tax incentives. That will likely lead to a sharp reversal in 2020. Meanwhile, plug-in vehicles already represent 56% of the market in Norway, so Tesla doesn’t have the same runway for growth that it enjoys in other countries where EVs are still a small (but fast-growing) piece of the market.

Perhaps the company can gain a better foothold in Germany thanks to the new Gigafactory. That market clearly holds a lot of potential. In addition to being the largest country in Europe, the government recently increased incentives for EV purchases. Still, German automakers will undoubtedly mount a stiff challenge to Tesla in their home market. With growth likely to slow in Tesla’s top two European markets, I expect the company’s sales in Europe to continue to trail its U.S. sales by a wide margin for the foreseeable future.

Wait for a pullback

Momentum could continue to carry Tesla stock higher in the near term, especially if the company projects another year of ~50% growth in deliveries for 2020 in conjunction with its Q4 earnings report. But the company will eventually have to back up the hype with spectacular revenue growth and margin improvement to justify its current market cap of nearly $100 billion.

Tesla clearly has plenty of room to grow. An expanded vehicle lineup (starting with the Model Y later this year) and the launch of local production in China and Europe will give it a good chance to grow annual sales to around 1 million units over the next 3-5 years.

Yet, even that level of output isn’t likely to generate enough profit to justify Tesla’s current valuation. After all, with 367,500 deliveries in 2019, the company is on track for roughly breakeven earnings on a full-year basis, even excluding stock-based compensation, which is nearing $1 billion annually.

If everything goes perfectly, Tesla stock could deliver spectacular returns over the next decade, even from its current starting point. However, with various impediments likely to offset some of the growth potential from its expanded vehicle lineup and global production footprint, long-term investors should stay away from the stock unless/until it surrenders most of its gains of the past three months.

If you enjoyed this article, please scroll up and click the “Follow” button to receive updates on my latest research covering the airline, auto, retail, and real estate industries.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

%

source https://jobsearchtips.net/tesla-stock-has-come-too-far-too-fast/

No comments:

Post a Comment