( Reuters) – The Federal Reserve’s bond portfolio is swelling once again at a rate not seen because the “quantitative easing” heyday in the early 2010 s. Rates for stocks and other dangerous possessions are also rising at a fast clip – a state of affairs that a growing chorus of financiers, financial experts and previous Fed officials state is no coincidence, and possibly a problem.

FILE PICTURE: The Federal Reserve building is envisioned in Washington, DC, U.S., August 22,2018 REUTERS/Chris Wattie/File Image

Considering that the Fed began purchasing $60 billion of Treasury costs a month last fall to counter ructions on short-term money markets, credit spreads are tighter and the bank financing markets targeted by the purchases are calmer. Financial tension steps tracked by regional Fed banks are at their least expensive in a year or more – all indications of the program’s success.

The S&P 500 also is up more than 10%since October.

Everything sets the phase for the very first difficult maneuver the Fed will undertake this year: switching off the tap. A misstep could have agonizing repercussions.

” The risk is what takes place when the Fed stops increasing their balance sheet,” stated Peter Boockvar, primary investment officer with Bleakley Advisory Group. “What will stocks do when that liquidity spigot stops? We’ll need to see.”

In the wake of the financial crisis of 2007-2009, the reserve bank acquired a vast portfolio of Treasuries and mortgage-backed securities – topping $4.5 trillion at its peak – through three operations referred to as quantitative easing, or QE.

While designed to help raise the economy after the crisis by holding down long-lasting interest rates, QE likewise had a side-effect that seems replaying now: Costs for risky assets like stocks and low-quality business bonds increased as the Fed’s portfolio grew.

GRAPHIC: The Federal Reserve’s balance sheet – here

” QE LITE”

Fed Chair Jerome Powell and other policymakers have asserted their latest balance sheet expansion is a technical adjustment and not stimulus. “Our Treasury costs purchases need to not be confused with the large-scale asset purchase programs that we released after the monetary crisis,” Powell said after October’s policy conference.

Lots of market watchers aren’t purchasing it, and numerous have dubbed it “QE Lite.”

” You can dispute it all you desire, however as long as the circulations are increasing the size of the balance sheet, stocks are going to rise in cost,” said Danielle DiMartino Cubicle, founder of Quill Intelligence, a boutique research company, and a past advisor to previous Dallas Fed President Richard Fisher.

Fisher, who ran the Dallas Fed from 2005 to 2015, stated the influence on markets might be driven mainly by expectations created during earlier rounds of QE, which referred hefty stock exchange gains.

” Markets view things and they might perceive things various than what you intend,” Fisher said, indicating a strong correlation in between the boost in the size of the Fed’s balance sheet and the increase in stock prices. “However there’s also a real impact.”

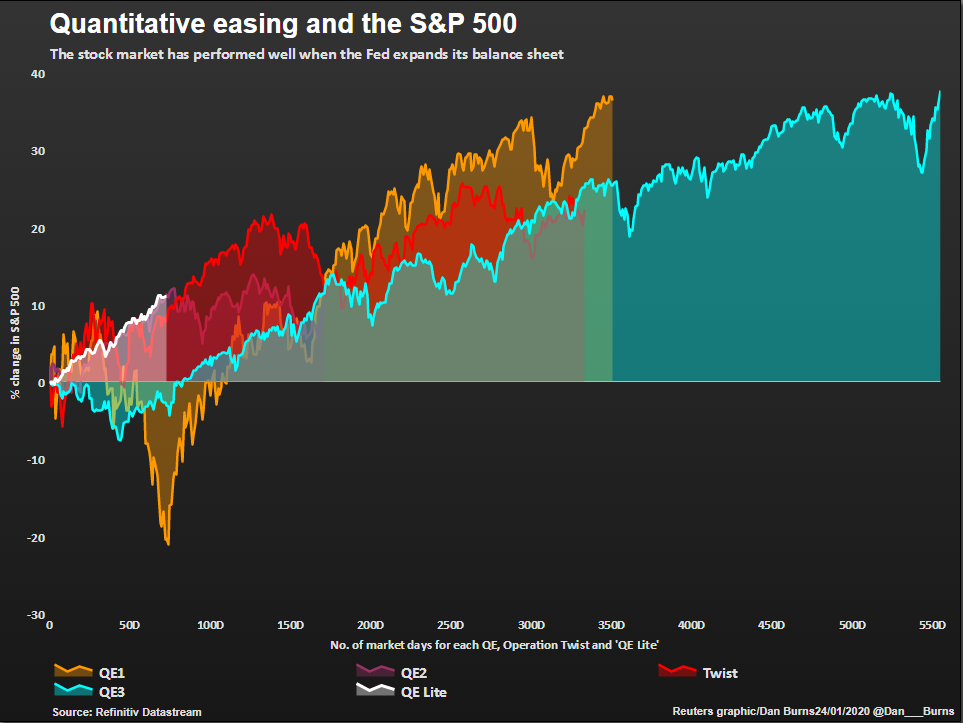

The S&P rose roughly 37%during both QE1 and QE3, and by 10%under QE2, which was the smallest operation of the 3. It has gotten 11%given that the brand-new T-bill purchases were announced.

Not everybody is convinced the Fed should get credit for the stock rally, pointing to an easing of trade tensions with China and greater optimism about the U.S. economy.

” Rather, the primary causes of the upturn in the stock exchange considering that October have probably been signs of economic healing at home after a short-term downturn throughout much of 2019,” John Higgins, chief markets economist for Capital Economics, composed in a research study note to clients.

GRAPHIC: Quantitative easing and the S&P 50 – here

FINDING THE RIGHT BALANCE (SHEET)

In a sense, the Fed faces a predicament of its own making.

It jumped back into the bond-buying company in mid-October after a crucial corner of U.S. cash markets seized up. It was an episode most likely exacerbated by the Fed having allowed its balance sheet to shrink excessive in the post-QE era, which left a lack of reserves in the banking system.

The current effort is created to replenish those drained reserves, which fell by 50%from their peak level of about $2.8 trillion at the end of QE3 in late 2014 to $1.4 trillion last September. They have given that rebounded and are nearing $1.7 trillion thanks to the fastest speed of asset accumulation since the early days of QE3.

The Fed has been unclear about the length of time the current program will run however has said the T-bill purchases will continue into the second quarter.

So a choice on calling time on “QE Lite” is rapidly approaching, though it is not clear if policymakers are prepared yet to announce their strategies. It will certainly be discussed as they gather in Washington on Jan. 28-29 for their very first conference of the year, and the perception that it has become a stimulus program is fretting for some.

Dallas Fed President Robert Kaplan stated previously this month he understands concerns the costs purchases may be increasing risky possessions and said officials should try to restrict development of the balance sheet.

” It’s one of a number of aspects that I think might be exacerbating the appraisal of dangerous properties, so as a main lender I have to be cognizant of it,” he stated.

Minneapolis Fed President Neel Kashkari stated on Twitter that he didn’t understand the link between the Fed’s costs purchases and the recent market gains. “Someone explain how swapping one short-term threat free instrument (reserves) for another short-term danger free instrument (t-bills) leads to equity repricing,” he tweeted. “I do not see it.”

Nevertheless, monetary markets have actually responded inadequately to some previous signals from the Fed on ending balance sheet development, most notably the so-called “taper tantrum” of 2013 when then-Fed Chairman Ben Bernanke indicated the reserve bank was preparing to slow the rate of its bond purchases as it wrapped up QE3.

Stocks sold off and, more importantly, bond yields rose, undoing the wanted effect of the Fed’s bond purchases, stated Roberto Perli, establishing partner and head of global policy research study at Foundation Macro, a research firm.

Now, though, the Fed is not attempting to influence bonds, and the possessions seeing the biggest upside are stocks, Perli stated. Any response this time is likely to be included there.

GRAPHIC: Bank reserves held at the Fed – here

Reporting by Jonnelle Marte; Editing by Dan Burns and Andrea Ricci

%.

source https://jobsearchtips.net/feds-very-first-difficulty-in-2020-ignoring-qe-lite/

{kind=link}

{kind=link}

{kind=link}

No comments:

Post a Comment